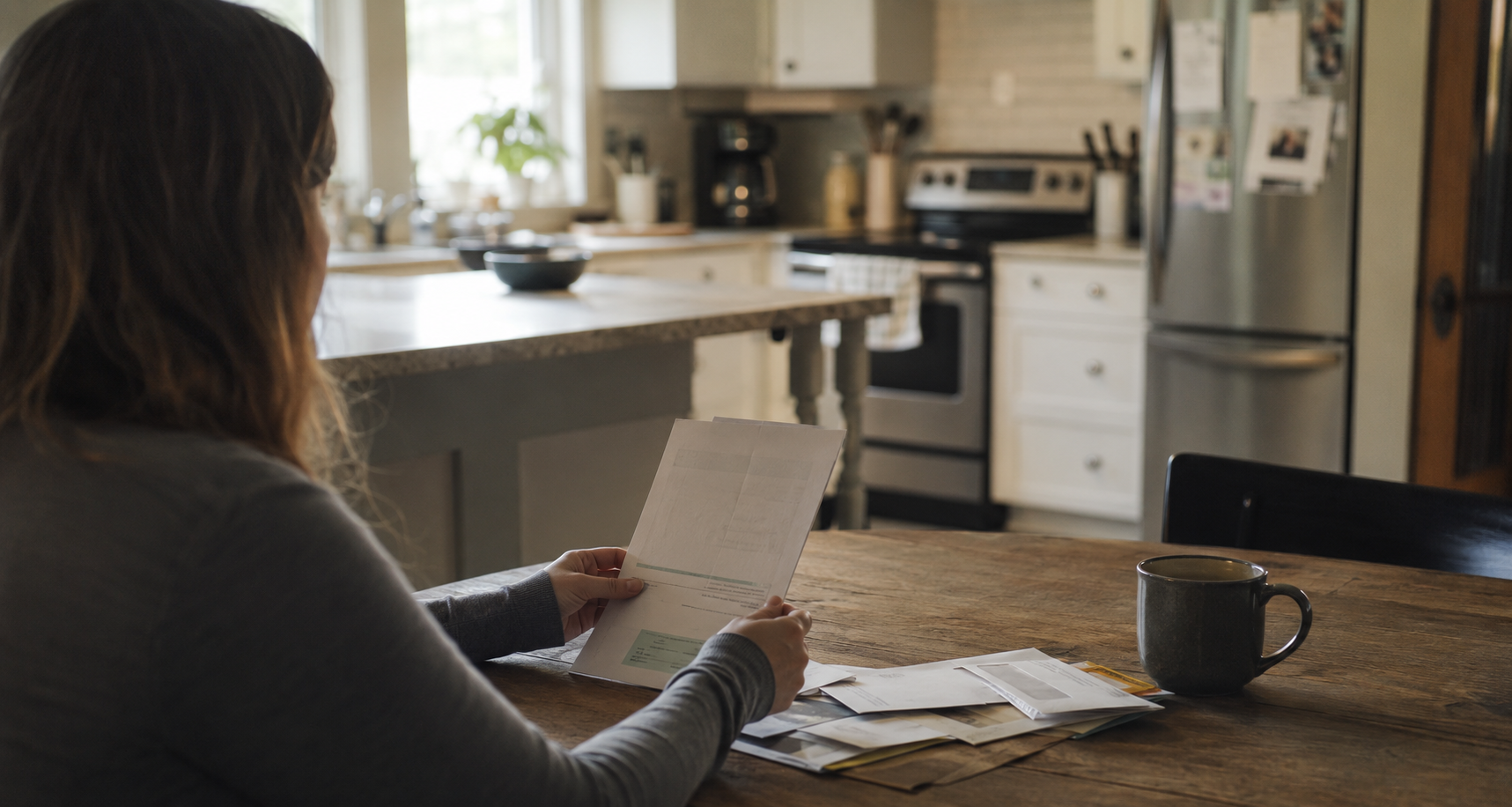

The cost of homeownership has quietly shifted from the mortgage to everything else. Insurance premiums are up 72% since 2019, property taxes are up 31%, and 20.7 million homeowner households are now spending more than 30% of their income on housing costs. The maintenance record has become the financial document that protects everything behind it.

For decades, the financial conversation around homeownership has centered on one number: the mortgage payment. Could you qualify? Could you afford the monthly payment? Was your debt-to-income ratio within range? The mortgage was the gate — and once you were through it, the hard part was supposed to be over.

That assumption is no longer accurate. The hard part, for millions of American homeowners, has moved to the back half of ownership. And it is getting harder.

What the numbers say

Harvard University's Joint Center for Housing Studies released its 2026 State of the Nation's Housing report in June, and the data on the ongoing costs of ownership is stark. Property taxes rose 31 percent between 2019 and 2025, while average monthly home insurance premiums jumped 72 percent — driven by extreme weather events and climate-related damage that is inflicting greater and greater losses on the nation's housing supply.

The cumulative effect is significant. As of 2024, 20.7 million homeowner households — 24 percent of the total — spent more than 30 percent of their income on housing expenses. 9.6 million spent more than half. That is up roughly 4 million households from 2019. The mortgage for most of these homeowners has not changed. What changed is everything around it.

At the same time, homeowners are borrowing against their equity at the fastest pace in years. According to ICE Mortgage Technology's June 2026 Mortgage Monitor report, homeowners withdrew an estimated $47 billion in equity in the first quarter of 2026 — the highest first-quarter total since 2021. Nearly two-thirds of that second-lien volume came from borrowers who took out their primary mortgages between 2020 and 2022, preserving those low-rate first mortgages while tapping stored equity to cover costs. The pattern tells a clear story: homeowners are staying put, and they are using the equity in their homes to absorb the rising cost of keeping them.

The insurance problem specifically

The 72 percent jump in insurance premiums deserves more attention than it typically gets. Insurance is not just an ongoing cost — it is a financial backstop that is only as useful as the claim it covers. And claims can be denied.

Most homeowners are not aware of the maintenance exclusions written into standard policies. If damage to a roof, a plumbing system, or a structural component is deemed to have developed gradually due to deferred maintenance, insurers have grounds to deny the claim. The policy requires "sudden and accidental" damage — not a problem that accumulated because no one was paying attention.

When premiums are rising 72 percent and you are already cost-burdened, a denied claim is not a minor inconvenience. It is a financial crisis. The documentation that proves your home was actively and responsibly maintained is the thing that protects you in that moment — not the premium you paid.

What this means for how homeowners manage their homes

The shift in the cost structure of homeownership changes what responsible ownership looks like. When the mortgage was the dominant cost and homes were appreciating quickly, deferred maintenance was a manageable risk. You could absorb it in the transaction or in the appreciation. That cushion is thinner now.

When insurance costs 72 percent more and covers less than many homeowners expect, the maintenance record becomes an asset in its own right. It protects claims. It documents the condition of systems before they fail. It creates the paper trail that an insurer needs to see when a repair was not neglected but simply scheduled.

When property taxes are up 31 percent and homeowners are locked in to their current properties, the home you own is the asset you are holding for the long term. Every deferred repair compounds against a balance sheet that is already under pressure.

The gap nobody is measuring

There is no standardized, widely published measure of how well American homeowners are maintaining their properties or how many have a documented maintenance record. This is a genuine data gap. For a nation in which homeowner households represent 24 percent of all cost-burdened housing situations and the median home is 42 years old, the absence of any systemic tracking of maintenance documentation is its own kind of risk.

What we know anecdotally — from insurance claim disputes, from real estate transactions that fall apart after inspection, from homeowners who cannot answer basic questions about their own systems — is that the majority of homeowners do not have a maintenance record. They have memory, and scattered paperwork, and a rough sense of what has been done.

That is not sufficient when the financial stakes of homeownership are this high.

What Oply is built for

Oply is an AI-powered home maintenance platform designed specifically for the homeowner the current market has created — one who is staying put, managing rising costs, and needs their home to be understood rather than merely occupied. It tracks maintenance history, sets recurring reminders tied to real completion dates, saves trusted service professionals, and builds a digital record that compounds in value over time.

The documentation that Oply creates is not just organizational. In the current insurance environment, it is financial protection. A homeowner who can demonstrate consistent HVAC service, roof inspection history, and plumbing maintenance is in a categorically different position when an insurer reviews a claim than one who cannot.

The mortgage was never the whole cost of ownership. It was just the part everyone was focused on. The back half — insurance, taxes, maintenance, documentation — is where homeownership is now being won or lost. That is exactly the problem Oply is built to solve.

The bottom line

The question used to be whether you could afford to buy a home. Increasingly, the more important question is whether you can afford to keep the one you have. The answer depends less on your rate and more on how well you understand and protect what you own. That starts with maintenance, and it starts with a record.