On America's 250th birthday, the national conversation about homeownership is entirely about getting in. The median first-time buyer is now 40 years old, saving for a down payment takes nearly a decade on average and 65 years in New York City. But the harder, quieter problem — what happens to the home after you finally own it — is the part nobody is measuring or talking about.

America turns 250 today. Across the country, the housing stories being published this week share the same theme: it has never taken longer, cost more, or required more sacrifice to become a homeowner. The data supporting that theme is genuinely sobering.

According to a new Realtor.com analysis released this week, the median age of a first-time homebuyer climbed to 40 years old in 2025 — the highest ever recorded according to NAR data — up from 30 in 1990. The time required to save for a down payment has stretched from roughly three years to nearly a decade. First-time buyers now comprise just 21 percent of all home purchases in 2025, a historic low — a contraction of 50 percent since 2007.

The math in some markets has become almost surreal. According to Rocket Mortgage's analysis of 49 major metros, a typical household in New York City would need 65 years to save the median first-time buyer down payment of $265,000 — about 30 percent of the typical purchase price in that market. In Detroit, the same exercise takes 3.9 years.

The system is stacked against people buying primary residences specifically. The average down payment for first-time buyers was 10 percent in 2025, according to NAR, while repeat buyers averaged 23 percent. Research from the Federal Reserve Bank of St. Louis found that in 2024, the median down payment from those buying a primary residence was 9 percent — compared to 25 percent for buyers of second homes or investment properties — and mortgage applications for owner-occupied primary residences were denied more frequently than applications for investment properties.

All of this is the story being told on America's 250th birthday. It is an important story. It is not the whole story.

The part nobody is talking about

Once you get the keys — after the decade of saving, the 40 years of life it took to get there, the mortgage application, the closing costs — something happens that the housing conversation almost entirely ignores.

Not in the abstract. In the specific. You have to know when the HVAC was last serviced, who installed the water heater and when, whether the roof has been inspected since the sellers owned it, which contractor did that electrical work two years ago, and when to flush the water heater before the sediment buildup shortens its life by years.

You have to do all of that while working, raising a family, managing the finances, and handling everything else that comes with the life you were building during the decade you spent saving.

And almost no one prepared you for it.

The costs that come after the mortgage

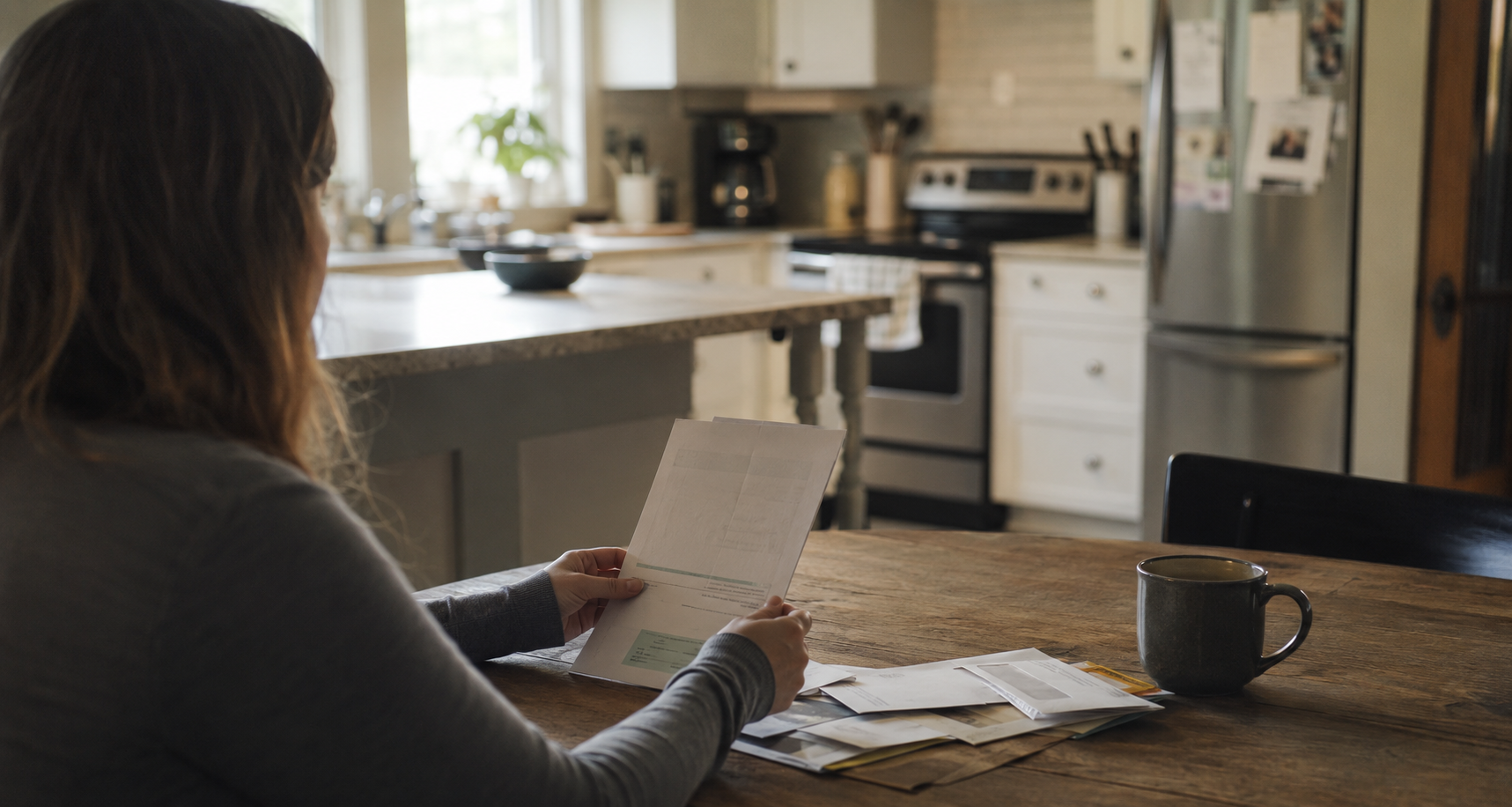

The financial picture of homeownership doesn't improve once you are in. According to Harvard University's 2026 State of the Nation's Housing report, property taxes rose 31 percent between 2019 and 2025, while average monthly home insurance premiums jumped 72 percent — driven by extreme weather events and climate-related damage inflicting greater losses on the nation's housing supply.

At the same time, 20.7 million homeowner households — 24 percent of the total — spent more than 30 percent of their income on housing expenses in 2024. The mortgage is one part of that. Insurance, taxes, maintenance, and repairs are the rest. And unlike the mortgage, those costs are not fixed.

A Redfin Premier agent in the Detroit area put it plainly: "I always tell my first-time homebuying clients to consider finding a home that's under budget so they can reserve funds for the additional costs of owning a home, such as regular maintenance and unexpected repairs, which can amount to tens of thousands of dollars. Many first-time home buyers previously had landlords who took care of all of that."

Most first-time buyers at 40, after a decade of saving, do not have a reserve for tens of thousands of dollars in unexpected repairs. They have a mortgage payment that stretched the limits of what they could qualify for.

The data gap nobody has filled

Here is the part that is genuinely surprising given how much data exists on getting into homeownership: there is almost no standardized, published data on what happens after.

We know the median age of the first-time buyer. We know the median down payment percentage. We know denial rates and income-to-price ratios and months of housing supply down to the decimal.

We do not know how many homeowners have a maintenance record for their property. We do not know how many can identify the age of their major systems. We do not know how many have a documented history of service that would protect an insurance claim from denial or support a cleaner transaction when they eventually sell.

The U.S. housing supply gap has reached approximately 4.03 million homes, and regulation adds more than $130,000 to the cost of a newly built one. Those are the numbers that drive the political conversation. The number that no one is tracking — how well Americans are actually managing the homes they already own — may matter just as much.

What the 250th anniversary should actually be asking

Every founding-anniversary housing story this week asks the same question: how do we help more people get in? That is the right question. It is not the only one.

NAR estimates that a 10-year delay in homeownership could mean losing roughly $150,000 in equity on a typical starter home over a lifetime. That is a real cost of the access problem. But there is a parallel cost that no one is quantifying — the equity lost, the claims denied, the systems that failed early, the homes that sold for less — because owners who finally got in had no system for managing what they owned.

The American Dream has always been framed as the moment of getting the keys. A home at 40, after a decade of saving, after fighting through a market stacked against owner-occupants, is a genuine achievement worth celebrating. But the home you get the keys to at 40 is a 42-year-old structure on average, with aging systems, a maintenance history you may not fully understand, and costs that will keep climbing regardless of what Washington does about supply.

Getting in is the beginning. Keeping it is the work.

Where Oply fits

Oply is an AI-powered home maintenance platform built for the homeowner the current market has created — one who got in later, paid more to get there, and needs the home they fought for to be understood, documented, and managed over time.

It tracks maintenance history, sets recurring reminders tied to real completion dates, saves trusted service professionals, and builds the kind of digital record that protects an insurance claim, supports a cleaner sale, and compounds in value the longer you stay. Not a marketplace. A system of record for the home you own.

America is 250 years old today. Homeownership remains one of its most powerful economic institutions. The conversation about how to make it more accessible is long overdue and increasingly urgent. The conversation about what happens after you get in — how you manage an aging asset, how you document what has been done, how you protect the investment that took a decade to make — is barely beginning.

That is the problem Oply is building toward.

Happy 250th, America. Now let's talk about what happens after you get the keys.