Owning a Home Now Costs $28,596 a Year. Here's What's Driving It.

The Wall Street Journal just put numbers to what every homeowner already feels: owning a home is getting significantly more expensive, in every direction, all at once.

The annual cost of homeownership — mortgage, taxes, insurance, maintenance, and repairs — hit $28,596 in 2025. In 2019 that same number was $20,618. That's a 39% increase in six years, outpacing inflation by a wide margin.

Here's what's actually driving it, and more importantly, what you can do about the parts you can control.

The Numbers Are Worse Than They Look

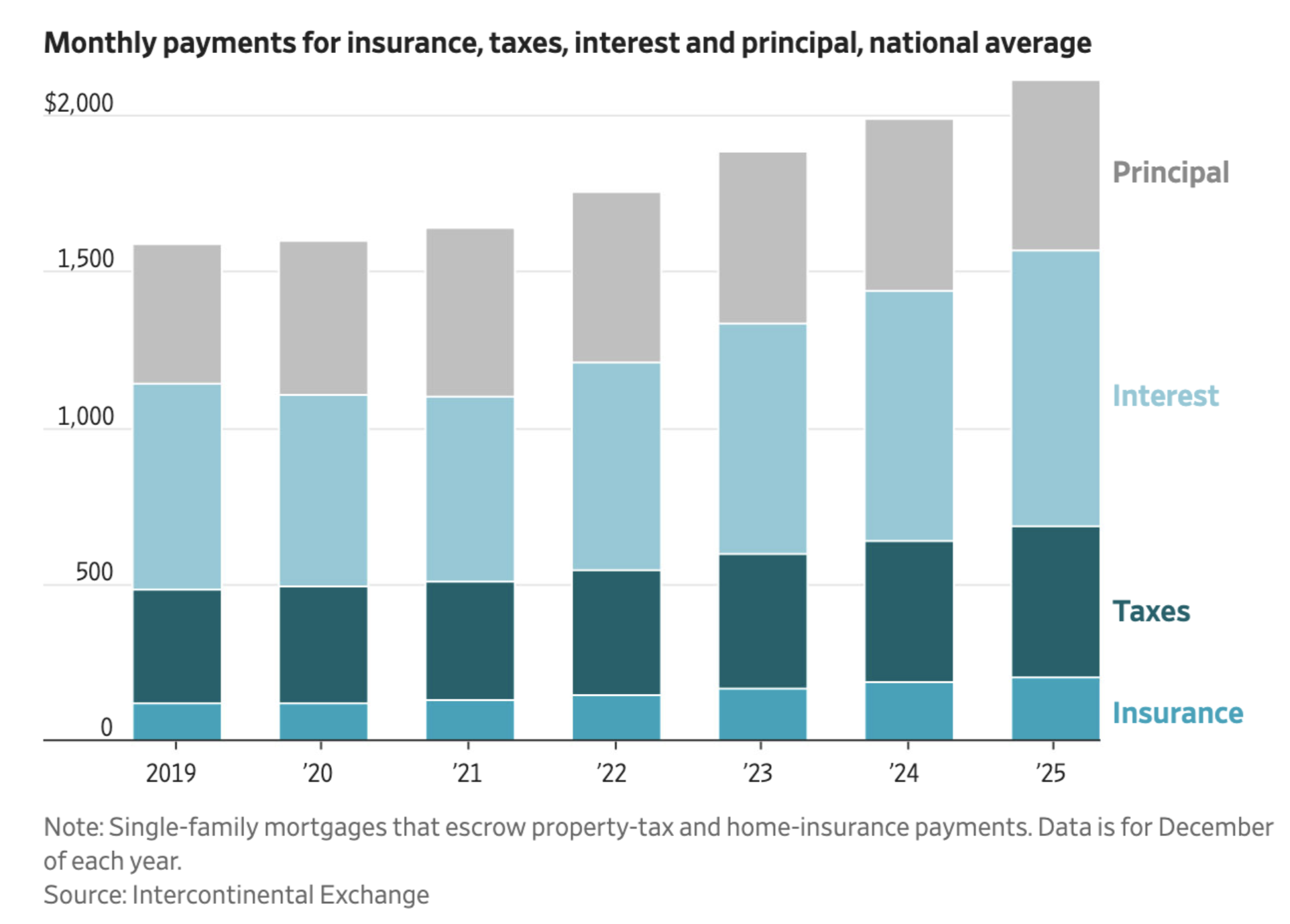

The headline figure — $28,596 a year, or roughly $2,383 a month before you spend a dollar on anything inside your home — is striking enough. But the breakdown is where it gets really uncomfortable.

Emergency repairs are up 175% since 2019. Not 175 dollars. 175 percent.

Home maintenance costs are up 85%. Insurance is up 72%. Property taxes up 31%. Interest up 35%.

The only category that hasn't gone haywire is principal — up 22%, largely because home values have risen. At least that one is building equity.

But emergency repairs up 175%? That number deserves to sit for a second. It means the average homeowner in 2025 is spending nearly three times what they spent in 2019 on problems that came out of nowhere and couldn't wait. A burst pipe. A failed HVAC in July. A roof leak that turned into a ceiling problem.

These aren't discretionary expenses. You don't get to say no.

Why Emergency Repairs Are the Most Important Number on That List

Of all the costs in the WSJ analysis, emergency repairs are the one that homeowners have the most ability to influence.

You can't control mortgage rates. You can't control what your county assessor decides your home is worth. You can't control what insurance companies are charging in a market rattled by natural disasters and rising labor costs.

But you can control whether small problems become expensive ones.

The reason emergency repair costs are up 175% isn't just because labor and materials cost more — though they do. It's because deferred maintenance compounds. A $200 maintenance task ignored for two years becomes a $2,000 repair. A $400 repair ignored becomes a $6,000 emergency. The math on neglect has always been brutal. At today's labor and material costs, it's devastating.

This is the core problem Oply was built to solve. Not the mortgage rate. Not the tax assessment. But the silent accumulation of deferred maintenance that turns manageable costs into financial emergencies.

The Cost You Can't See Coming

Here's the thing about emergency repairs: they feel random. Your water heater dies. Your furnace goes out in February. Your sump pump fails during a heavy rain.

But most of these "emergencies" have warning signs. They just happen slowly, quietly, in places you don't think to look until it's too late.

Water heaters fail early because nobody flushed the sediment or replaced the anode rod. HVAC systems fail because filters weren't changed and the system ran stressed for years. Roofs develop leaks that become structural problems because gutters weren't cleaned and water backed up. Pipes burst because nobody addressed the insulation gap in the crawl space.

The 175% increase in emergency repair costs is, in large part, a deferred maintenance bill that finally came due. And at 2025 labor rates, it's a big one.

What You Can Actually Control

The four cost categories in the WSJ analysis you can't change: mortgage rates, home values, insurance markets, and property tax assessments. Those are macro forces. You're along for the ride.

The two you can influence directly: maintenance and emergency repairs.

And the lever that controls both is the same: staying ahead of your home's maintenance schedule before small problems become expensive ones.

That doesn't mean spending more money. It means spending the right money at the right time. A $30 anode rod replacement every three to five years versus a $1,200 water heater replacement. A $25 HVAC filter versus a $4,000 emergency service call in the middle of summer. A $15 tube of caulk versus a mold remediation bill you don't want to know about.

The math on proactive maintenance has always been favorable. At today's repair costs, it's not even close.

The Bigger Picture

The WSJ analysis also points to something important happening in the housing market overall. Home sales have been stuck around 4 million a year since 2023 — the lowest level in decades. Homeowners who want to move can't afford to buy at today's rates and prices. New buyers are stretching budgets thin to get in. Everyone is more financially exposed than they were five years ago.

That means the cost of an unexpected $5,000 repair hits harder in 2025 than it did in 2019. There's less buffer. Less margin for error. The financial case for staying on top of your home has never been stronger.

The One Thing to Do Today

If you read this and feel a little anxious about your home — that's the right response. But anxiety without action doesn't help anyone.

The most practical thing you can do right now is take stock of what you actually know about your home. When was your water heater last serviced? How old is your HVAC? When did you last check the pressure relief valve? When was the last time someone looked at your roof?

Most homeowners can't answer those questions. Not because they don't care about their home — but because there's no system for tracking it. No reminder. No record. Just hoping nothing breaks.

That's what Oply is for. We track your home's systems and appliances, remind you when maintenance is due, and connect you to trusted pros when you need them. It's not a magic fix for rising mortgage rates or insurance premiums. But it's the most direct thing you can do about the two costs on that list that you actually control.

Your home is probably the most expensive thing you own. At $28,596 a year and rising, it's worth having a system for it.

Sources: Wall Street Journal, "See How Owning a Home Is Getting More Expensive in Every Way" (June 20, 2026).